Fico Scores Importance: How To Calculate And Evaluate Credit Score

Introduced by Fair Isaac Corporation (FICO), FICO scores are considered by the credit card issuer or credit lender to estimate how likely the creditor can repay if the lender grant...

Introduced by Fair Isaac Corporation (FICO), FICO scores are considered by the credit card issuer or credit lender to estimate how likely the creditor can repay if the lender grants credit. Fico score also known as FICO Credit Score determines the interest rate be set on the credit amount. The enhancements such as Tradelines take the proprietary formula to determine the credit worthiness.

When an Authorized User Tradelines applies for credit, whether it is for an auto loan, mortgage or credit card, a lender will execute the Credit Report. Fico Score is generated on the information of an authorized user credit report managed by credit agencies. The biggest benefits of FICO Credit Score, is it lowers the credit risk while it is highly used to the acceptance of providing credit.

Fico credit is used to the data of your credit reports by credit reporting agencies such as Equifax, Experian and TransUnion. The widely used three-digit score stays between 300 and 850. Generally, 740 range is considered as the excellent score quality of best rates.

WHAT ARE THE TYPES OF FICO CREDIT SCORE?

There are multiple FICO scores which depend on the lender to assess the borrowers considering on their loan product. Such as:

- Auto Loan: When a lender is taking the borrower for an auto loan will prominently be interested in auto loan payments history for a personal loan. There are 3 factors determine the monthly auto loan payments, these are how much you borrow, the interest rate you offer and terms of a loan. Fico Credit Scores is highly valuable for an auto lender.

- Mortgages Loan: FICO Score are influenced by interest rates. Authorized User Tradelines can help you qualify for mortgage loans.

- Credit Cards: Use of credit card leaves an important impact on FICO Score. This one is the most renowned reason to choose a Tradelines which helps to evaluate the credit history and results to Fix Poor Credit Rating by boosting credit score fast.

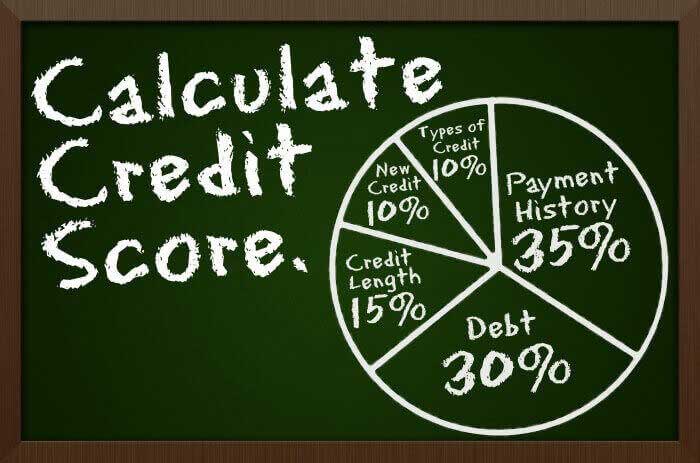

HOW TO CALCULATE THE FICO SCORES

Since 1989 the Fico Scores get updated to the new version, presently FICO 9 Vs FICO 8 are considered to evaluate the credit report. In order to calculate the FICO Scores, below factors are considered:

Payment History (35% of Your Score): Payment history is considered to find the payment scale, whether the applicant has made all payment on time or not. Late payment may affect your credit score negatively. A bankruptcy in collections may also hurt you.

Credit Limit (30%): It refers to the amount of credit how much currently used by the lender. The less it is, the better it is for your score.

Credit Age (15%): How old your credit is, it highly depends on your credit score. Generally, a credit account should be at least 6 months older to be calculated in FICO Credit Score.

Last Application for Credit (10%): When you apply for the new credit, you may go through the hard inquiry for at least six months.

A Number & Type of Credit Account (10%): If you have both instalment credit account and revolving credit account, it helps to your Fico Credit Score.

HOW TO EVALUATE THE FICO CREDIT SCORE

However, when you choose to improve your credit score, you have to make quick and fast efforts because it is not an easy task to Boost Credit Score Overnight by yourself. Still, if you follow the below tips, you will definitely get Rapid increase to your Credit Score. The major tips are:

- Check credit Report after the certain time period

- Set the payment reminders

- Reduce the amount of debt you lend

- Make payment of all bills on time

- Prevent your account from paying off a collection account

- Keep the lower balance on credit cards

- Pay off the debts instead of closing the account

- Don’t open new accounts altogether or rapidly

FICO score is calculated on the basis of the credit report. Fair Isaac Corporation has not leaked the information on how exactly the FICO Score is calculated one must consider the above described respective suggestion to Raise Your FICO Score. Still, if anyone is facing any problem then take help of Tradelines Broker to get the best way on how to evaluate your credit score.